If you’ve used our comparison tables to compare loan products, you’ve probably noticed we show two rates per loan product. You might be a bit confused about what the difference is, so we’ve broken it down for you.

Essentially, the advertised rate determines your regular repayment, whether that’s weekly, fortnightly, or monthly. However, it doesn’t take into account any extra fees. This is where the comparison rate steps in, and can be considered a more realistic representation of the true cost of the loan.

Understanding both comparison and interest rates is crucial when you're shopping around for a loan. The interest rate alone doesn’t always reflect the full cost of borrowing. The comparison rate helps cut through the noise and provides a more realistic snapshot of what you’ll actually pay over time.

What is a comparison rate?

A comparison rate is a single percentage figure that combines the loan’s advertised interest rate with most of the associated fees and charges. It’s a standardised calculation based on a $150,000 loan over 25 years. This might be considered outdated given the average loan size is more than quadruple this and mortgages are now often repaid over 30 years.

However, the comparison rate gives you a clearer picture of the true annual cost of a loan, making it easier to compare offers side by side. Think of it as the “real” cost of a loan, expressed as a percentage.

For example, a home loan with a low advertised interest rate might seem appealing, but once you factor in extra fees, it could end up being more expensive than a loan with a slightly higher rate and fewer costs.

If both Lender A and B have an advertised rate of 5.00% p.a. but Lender A has a comparison rate of 6.00% p.a. while B’s is 5.50% p.a. you can assume the true cost of Lender A’s product is more expensive.

Why is the comparison rate higher than the advertised rate?

Most loans include additional costs that aren’t obvious at first glance. So if you’re in the market for a home loan, don’t be fooled by the headline rate alone. It’s the extra fees and charges that cause the comparison rate to sit higher. Here are some of the most common ones:

-

Application fee - a one-off fee charged by the lender when you first apply for a loan, covering paperwork and loan setup costs.

-

Monthly fee - a recurring service charge added to your loan each month, usually for account maintenance.

-

Annual fee - a yearly charge for keeping the loan active, often tied to package loans that include added features.

-

Redraw fee - a fee charged when you access extra repayments you’ve made on your loan via a redraw facility.

-

Offset fee - a fee for having an offset account linked to your loan, which helps reduce interest by offsetting your balance.

-

Package fee - a bundled fee covering multiple loan features or banking products, like credit cards or savings accounts, under one home loan package.

-

Discharge fee - a fee paid when you fully pay off your loan or refinance, covering the cost of closing your loan account.

-

Valuation costs - fees for the lender to assess the market value of the property you’re buying, which helps determine how much they’ll lend you.

-

Settlement costs - fees related to finalising the home loan and property transfer, including legal and administrative charges.

-

Revert rate - the interest rate a fixed home loan reverts to once the period is up (anywhere from 1 to 5 years). Revert rates are often much higher and are encompassed into the comparison rate.

Your lender might not charge all of these, but a few. That’s why relying solely on the advertised rate can be misleading. The comparison rate is a smarter, more accurate way to judge the total cost of a loan and often reveals which deal is truly better in the long run.

However, very few customers stick with the same lender and product for an entire 30 year period. Many refinance or pay off their loan early. This means that certain fees might not matter to one customer as much as others; this is why it can be important to look at the fees payable and a loan’s key facts sheet, as well.

Interest rate vs comparison rate

Looking at the comparison rate can be useful because it levels out the playing field. Some lenders like to offer seductively low interest rates only to sting you with a lot of expensive fees every year. In this case, picking one with a higher interest rate yet fewer fees could be more economical in the long run. Some lenders charge few, if any, fees. You can see a basic scenario below.

|

Home Loan A |

Home Loan B |

|

|---|---|---|

|

Advertised Rate p.a. |

5.30% |

5.50% |

|

Regular Monthly Repayment on $400,000, 25 year term |

$2408 |

$2456.35 |

|

Comparison Rate p.a. |

5.80% |

5.55% |

|

Fees payable p.a. (averaged out over 25 years) |

$2000 |

$200 |

|

Total cost on average per month |

$2574 |

$2473 |

Presumably you would lean towards the one with the lower rate. However, loan A has a large processing fee, as well as expensive annual fees, and when you include these costs, it means you’ll actually end up paying more per year.

Loan B on the other hand, has very few such costs. A 5 basis point difference on the comparison rate is $200, which might be for an annual fee. So even though it has a higher advertised rate, which is a turn off, it’s the relative lack of fees that slightly win in the end.

While a low advertised interest rate might catch your eye, it doesn't always mean you're getting the best deal. Below is a real-world comparison among home loans currently offered by major lenders. Make sure you’re mindful of the comparison rate and any terms or conditions that may significantly impact the overall cost.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Extra Repayments | Split Loan Option | Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

6.04% p.a. | 6.08% p.a. | $3,011 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | ||||||||||

5.89% p.a. | 5.80% p.a. | $2,962 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | ||||||||||

6.04% p.a. | 6.07% p.a. | $3,011 | Principal & Interest | Variable | $0 | $799 | 80% |

| Promoted | Disclosure |

Comparison rate lower than the advertised rate?

You might have seen a few home loans with comparison rates lower than the advertised rate. This is relatively uncommon as it’s usually the other way around. Keep in mind that this doesn’t necessarily indicate there’s no fees to pay. It’s usually down to three main reasons:

1. Fixed-rate loans with a lower revert rate

Some fixed-rate home loans revert to a lower variable rate once the fixed period ends. Since the comparison rate blends the fixed period with the revert rate over the life of the loan, it can bring the average (i.e. the comparison rate) down.

2. Loyalty or ongoing customer discounts

Lenders sometimes apply ongoing interest rate discounts for loyal customers or package deals. These discounts may not be reflected in the initial advertised rate but are built into the comparison rate.

3. Interest-only construction loans

Construction loans often start with interest-only payments during the build phase and then revert to a lower principal and interest (P&I) rate once construction is complete. The advertised rate might reflect the higher initial phase, while the comparison rate averages out the lower P&I phase that follows.

How is the comparison rate calculated?

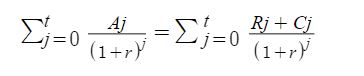

Section 71 of the National Consumer Credit Protection (NCCP) Act requires lenders to use a standardised formula to work out the comparison rate, and it’s not exactly straightforward. The comparison rate is calculated using the formula n x r x 100%, where n represents the number of repayments made per year (52.18 with weekly repayments and 26.09 for fortnightly) and r is the solution to, ahem, a much more complex formula as seen below:

where:

-

j=the number of intervals between repayments.

-

Aj=the outstanding loan amount at time j.

-

Rj=the repayment to be made at time j.

-

Cj=additional fees or charges that will apply when Rj repayment is due.

-

t=the number of intervals between repayments that will elapse throughout the entire loan term.

Feel like Rain Man yet? While your eyes might have immediately glazed over at this formula, it’s probably enough to just know that by law, a comparison rate is required to be the total amount you will pay each year, in both interest and fees.

Despite the algebra above, it’s not an exact science. Repayments aren’t usually uniform over an entire loan term, as on variable rates they can fluctuate; comparison rates might not encompass all fees payable, either. But it’s still a useful approximation. A more useful formula is probably: higher comparison rate = more $$$.

Limitations of comparison rates

If you’re choosing between loan products, comparison rates are usually a better way to work out which will be more expensive than just looking at the interest rate. However, there are several limitations of comparison rates that can mean you don’t end up paying exactly the amount the rate suggests.

Individual circumstances

Comparison rates are calculated based on a set of standard assumptions which may or may not reflect your situation. Credit history, the loan amount and the term length can all affect the costs and repayment terms for an individual.

Historically, banks have used a $150,000 loan size on a 25 year term as a yardstick to determine the comparison rate. However, that seems woefully out of date, because the average home loan size is well over $600,000 and most people take out a 30-year term, but pay it off in much less. Our comparison tables use $400,000 as a guide, as you will see in the disclaimer.

Variable fees

It’s possible to incur additional fees not included in the comparison rate calculation which would make the loan more expensive. Examples include:

-

Early repayment or break fees

-

Redraw fees

-

Late payment penalties

So if you’re interested in paying off your loan early or expect to make extra repayments, you’ll want to check these fees as well when comparing products, which won’t be included in the comparison rate.

Loan features

Many loans include features like offset accounts, redraw facilities or flexible repayment options, all of which can change how much you spend.

Two loans might have the same comparison rate, but very different features. If you use these features well, they could save you thousands over the life of your loan.

People chop and change lenders

How many people do you know who have stayed with a lender their entire 30-year loan term? Or taken the whole 30 years to pay it off? Many prioritise the home loan above all else, and work hard to pay it off much sooner. Further, many people refinance every few years to a better home loan deal.

So when you’re looking a lender, you’ll need to look at the specific fees payable. If you think you’ll refinance regularly, an annual fee might not be so important, but regular monthly fees could.

Where do you find the comparison rate?

Finding the comparison rate for a loan is fairly straightforward. In Australia, lenders are legally required to display comparison rates alongside the advertised interest rate for most home loan products. Here’s where you’ll typically find them:

-

On the lender’s website, next to the interest rate on product pages or in small print under promotional banners

-

On the key facts sheet for each home loan product provided upon request

-

From mortgage brokers if you’re working with one

-

From loan comparison websites where you can compare multiple home loans side-by-side